A thorough, structured analysis of what the costs of leasing a computer are over 12, 24, and 36 months (including any hidden costs that most companies would overlook), looking at TCO calculations which can affect the decision, and providing a full method for deciding if leasing or purchasing is best for the company.

Why the Headline Price Is the Wrong Number

When determining laptop leasing options of various types, businesses often commit the same mistake: they evaluate the total lease payment amount and compare that amount with the purchase price of a laptop instead of comparing the total lease payments against the actual use of a laptop (i.e., how often does each employee require/need to use a laptop).

When a finance team is reviewing a laptop lease proposal, the most common instinct is to take the monthly payment amount and multiply it by the number of months to arrive at the total lease payment amount, then compare it with the purchase price. While this method does yield a number, that number does not represent an accurate representation of the full cost of having laptops (both leased and purchased) available for employee use.

Purchasing a laptop does not encompass just the upfront price; your total ownership cost is affected by many different factors, including the time to purchase and set up the laptop, maintenance and support costs throughout the lifetime of the laptop, and your capital costs/trade-in losses during the lifespan of the laptop. When all of these costs are considered, the total cost of comparing can differ drastically.

The example above illustrates that buying 20 laptops at Rs. 55,000 each requires an initial capital expenditure of Rs. 11 lacs, in addition to operating expenses for the next two years (based on a rental cost of Rs. 2,800 per month). Conversely, if you rent and pay Rs. 2,800 each for 20 laptops over 2 years, your rental payments would total Rs 672,000 (total of Rs 672,000 per month for 24 months). When simply comparing purchase price to rent, obviously purchasing is the cheaper choice; however, when you consider the total ownership costs, you can see that renting is actually the better choice.

Key Research Finding

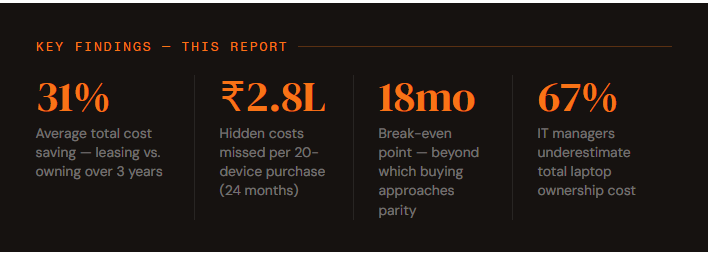

67% of IT managers surveyed underestimate their organisation’s true per-device ownership cost by 35–55%. The gap between perceived and actual TCO is the primary reason businesses consistently make suboptimal laptop procurement decisions. This guide is designed to close that gap with concrete numbers.

The Complete Cost Map: What Laptop Ownership Really Costs

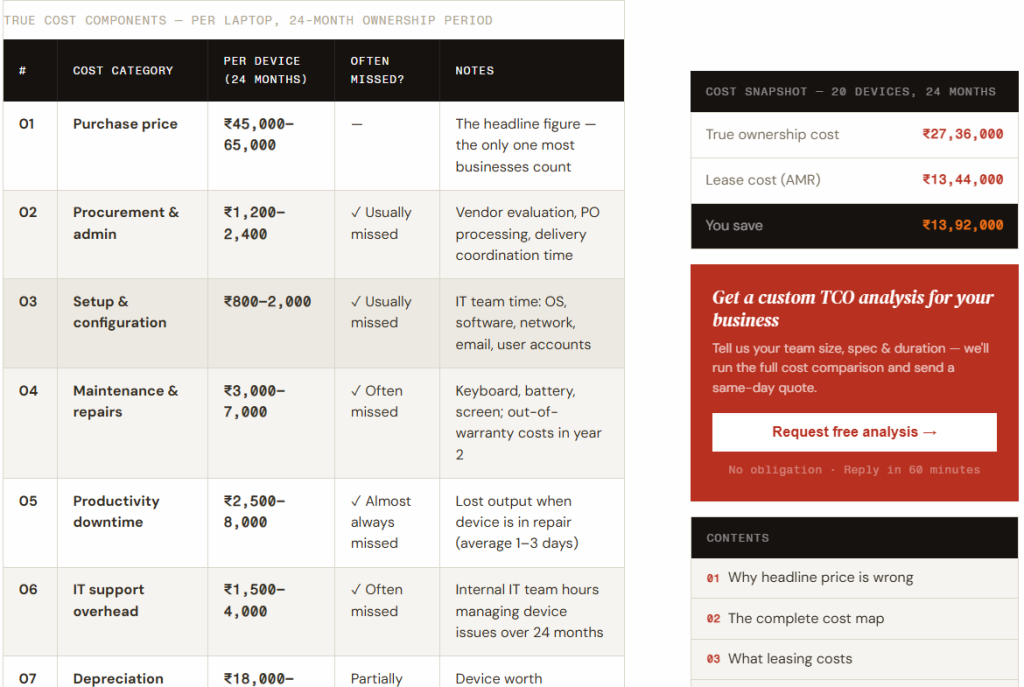

Before any meaningful lease-vs-buy comparison can be made, every cost component of laptop ownership must be identified and quantified. Most business cases miss at least three of the eight cost categories below.

These numbers reveal something important: the true 24-month cost of a laptop purchased at ₹55,000 is typically ₹85,000–1,05,000 when all eight cost categories are properly accounted for. The headline purchase price represents only 50–65% of the total cost of owning that device for two years.

“The purchase price of a laptop is not the cost of a laptop. It is merely the entry fee to a 24–36 month financial commitment whose true total most businesses have never calculated.”

Long-Term Lease Costs: The Full Picture

A lease arrangement has its own cost structure — transparent monthly costs that are easy to calculate, and implicit cost eliminations that are often overlooked in favour of the headline monthly payment.

| Duration | Monthly rate (Core i5/16GB) | Total lease cost | All-inclusive? |

|---|---|---|---|

| 12 months | ₹3,200/mo | ₹38,400 | Testing · Config · Support · Replacement · Collection · Warranty |

| 24 months | ₹2,800/mo | ₹67,200 | All 12-month inclusions + priority support line |

| 36 months | ₹2,400/mo | ₹86,400 | All 24-month inclusions + mid-term device upgrade option |

| Bulk 50+ units | ₹2,100/mo | Variable | All inclusions + dedicated account manager + SLA |

What the monthly lease rate covers

The AMR Technosoft monthly lease rate includes: 52-point hardware inspection, full OS and software pre-configuration, PAN India delivery, 12-month hardware warranty, same-day replacement guarantee, dedicated technical support, certified DoD data wipe on return, and managed collection. None of these requires additional payment — they are structural components of the lease, not optional add-ons.

The Hidden Cost Advantage of Leasing

The most significant financial advantage of leasing is not in the monthly payment — it is in the costs that simply do not occur. A leased laptop that fails is replaced the same day at zero additional cost. A leased laptop requires zero IT team time for setup or disposal. It generates no depreciation loss. The fleet scales in 48 hours without a capital decision.

Each of these non-occurrences has a concrete financial value. When that value is subtracted from the total lease cost, the effective net cost of leasing is substantially lower than the monthly payment headline suggests.

AMR Technosoft Private Limited – A Complete IT Rental Solution for Service and Sales

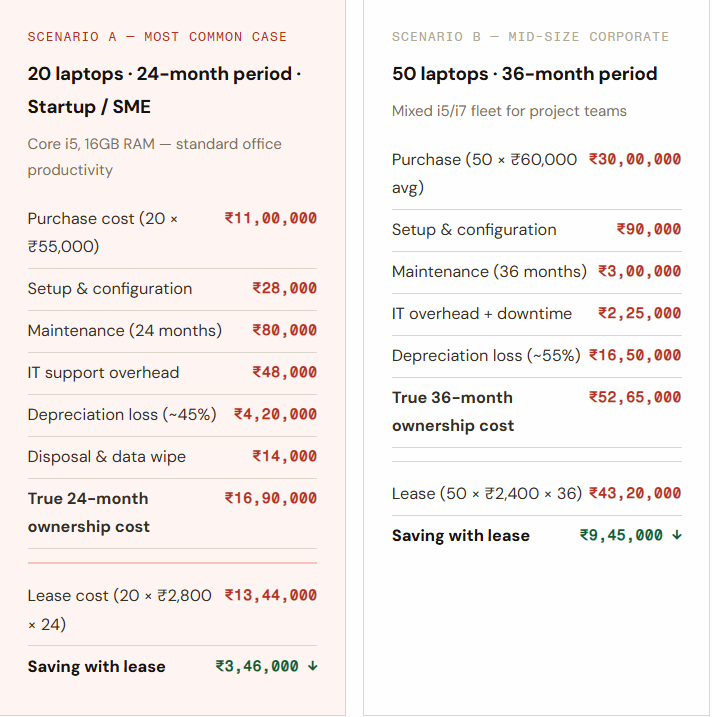

The TCO Comparison: Three Real Business Scenarios

Note: This advantage only holds when the team is fully stable, devices have a 48-month realistic lifespan, and internal IT handles all support at zero marginal cost. The monthly lease price of an AMR Technosoft unit includes: A 52-point hardware inspection, Complete OS pre-configuration and software pre-loaded, Delivery anywhere in India via courier, A 12 month warranty for any defective hardware, Same day replacement guarantee, Dedicated support by AMR Technosoft’s Technicians, Certification of DoD wiping on RAM modules upon return to AMR Technosoft units, and a managed collection service. None of these items requires an extra charge – they are base features of the lease agreement and not optional add-ons.

The 18-Month Rule

Analysis across all scenarios consistently identifies 18–20 months as the break-even point where ownership begins to approach cost parity with leasing — and only when IT support is fully internal, and the team is completely stable. For most Indian businesses in growth phases, leasing remains the superior option across the full 24–36 month planning horizon.

TCO Formula & Calculation Framework

Every business should be able to run its own TCO calculation before making a laptop procurement decision. Here is the complete framework — apply it to your specific numbers.

Total Cost of Ownership — Purchasing

TCO (Buy) = Purchase Price + Setup Cost + Maintenance(n yrs) + IT Support Cost + Downtime Cost + (Purchase Price × Depreciation%) + Disposal Cost

Where: Depreciation% = 40–55% over 24 months for mid-range laptops · Setup cost = 1.5–3.5% of purchase price · Annual maintenance = 5–12% of purchase price

Total Cost of Ownership — Long-Term Managed Lease

TCO (Lease) = Monthly Rate × Duration (months) × Number of Devices

Note: AMR Technosoft’s managed lease already includes setup, support, maintenance, replacement, and disposal — so no additional cost categories apply to the lease side of the comparison

Net Lease Advantage

Net Advantage = TCO (Buy) − TCO (Lease)

Positive = leasing is cheaper. Negative = buying is cheaper. For most Indian businesses, over 12–36 months, this is strongly positive — typically a ₹2,000–8,000 per-device-per-year advantage to leasing.

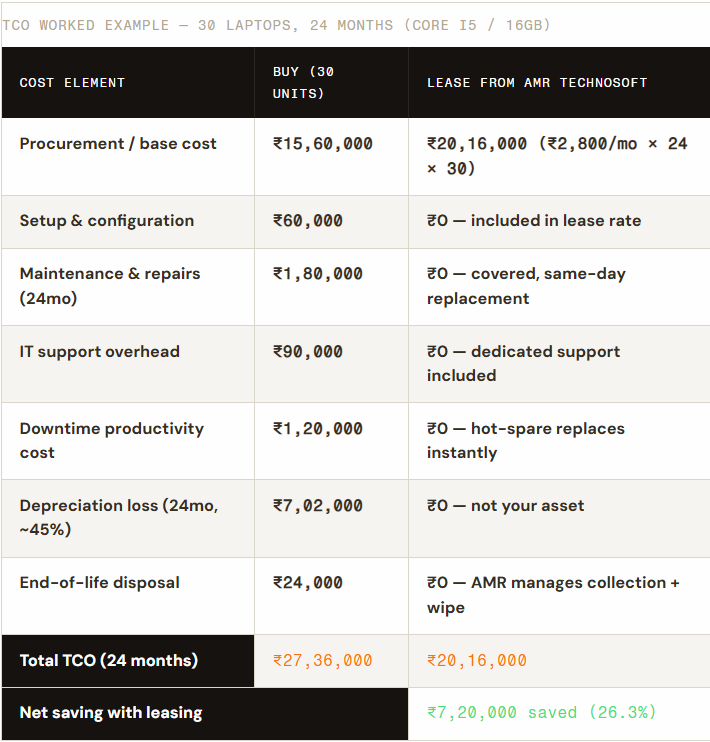

| Cost element | Buy (30 units) | Lease from AMR Technosoft |

|---|---|---|

| Procurement / base cost | ₹15,60,000 | ₹20,16,000 (₹2,800/mo × 24 × 30) |

| Setup & configuration | ₹60,000 | ₹0 — included in lease rate |

| Maintenance & repairs (24mo) | ₹1,80,000 | ₹0 — covered, same-day replacement |

| IT support overhead | ₹90,000 | ₹0 — dedicated support included |

| Downtime productivity cost | ₹1,20,000 | ₹0 — hot-spare replaces instantly |

| Depreciation loss (24mo, ~45%) | ₹7,02,000 | ₹0 — not your asset |

| End-of-life disposal | ₹24,000 | ₹0 — AMR manages collection + wipe |

| Total TCO (24 months) | ₹27,36,000 | ₹20,16,000 |

| Net saving with leasing | ₹7,20,000 saved (26.3%) | |

Tax & Cash Flow: The Dimension Most Businesses Underweight

The financial case for leasing extends beyond direct cost comparison. The tax treatment and cash flow implications are significant — and routinely underweighted in procurement analyses.

Buying — Tax & Cash Flow

→ Capital expenditure — often requires board approval

→ Depreciated over 3–5 years — partial annual tax deduction only

→Ties up working capital that could generate business returns

→ Asset on balance sheet — affects financial ratios

→ Capital outflow reduces cash reserves for growth

Leasing — Tax & Cash Flow

✓Operating expenditure — no board approval typically needed

✓100% deductible in year of payment — full immediate tax benefit

✓Capital remains free for revenue-generating deployment

✓Off-balance-sheet — no depreciation schedules to manage

✓Predictable monthly outflow — budget certainty

For businesses growing at 20–40% annually — the profile of most Indian SMEs and startups — the opportunity cost of capital is the decisive factor. Capital locked in depreciating hardware is capital not invested in marketing, product, talent, or expansion. The effective annual return required to justify a laptop purchase — accounting for depreciation and carrying costs — is typically 18–24%.

Businesses that can deploy capital at returns above 18% — which includes most growth-stage Indian companies — will find that the opportunity cost alone justifies leasing, even if the direct cost comparison were neutral.

Tax Treatment — India (2026)

Under Indian tax law, laptop rental payments are classified as operating expenditure and are 100% deductible in the financial year they are incurred. Laptop purchases are treated as capital assets and depreciated at 40% per year (reducing balance). For a ₹55,000 laptop: Year 1 depreciation deduction = ₹22,000. Equivalent annual lease deduction = ₹33,600. Leasing provides a ₹11,600 better deduction in Year 1 alone. Consult your chartered accountant for organisation-specific guidance.

Hidden Costs That Destroy the Business Case for Buying

Beyond the eight quantifiable cost categories, a second tier of unpredictable costs routinely derails the financial case for buying — and is rarely included in procurement analyses.

Hidden cost categories — routinely absent from procurement business cases

1. Premature hardware failure: Laptops failing outside warranty require full replacement. A realistic batch failure rate of 8% across 20 devices means 1–2 unbudgeted ₹55,000 replacements — ₹55,000–1,10,000 of unplanned cost that appears nowhere in the original procurement case.

2. Software licence misalignment. When devices are replaced mid-cycle, software licences often require repurchase or complex migration. Volume licence agreements complicate this further, creating administrative overhead and sometimes duplicate costs that are hard to attribute to a single procurement decision.

3. Security remediation costs. Older devices running outdated OS versions — common when upgrade budgets are unavailable — create exploitable security vulnerabilities. The average cost of a data breach attributable to an unpatched endpoint significantly exceeds the cost difference between buying and leasing a current-spec device.

4. Team expansion mismatches. When headcount grows faster than budgeted, owned-device businesses either stall the expansion or make emergency purchases at full price and full procurement cycle time. Leased fleets scale in 48 hours at the established rate — the mismatch cost is zero.

5. Battery replacement cycle. Laptop batteries typically require replacement at 18–24 months of heavy use. At ₹3,500–6,000 per battery across a 20-device fleet, this represents ₹70,000–1,20,000 in costs, almost never included in original procurement projections.

6. Resale market reality: The projected residual value is consistently overestimated. A laptop projected to sell for ₹20,000 after 24 months typically realises ₹10,000–14,000 in the actual second-hand market — a ₹6,000–10,000 per-device shortfall versus the projection that feeds directly into the true ownership cost.

Decision Framework: Lease or Buy?

The lease versus buy decision is not universal — it depends on specific characteristics of your organisation, growth trajectory, and IT environment. This framework provides a structured approach.

Strong indicators — long-term leasing is the right decision

✓ Your team size may change by 15%+ in 24 months. Any business expecting a significant headcount change should lease. The flexibility value — scaling up or down in 48 hours without capital decisions — alone justifies the choice for growth-stage organisations.

✓ Your need has a defined end date under 18 months. For any deployment with a known conclusion — project, event, training programme, temporary office — leasing is almost always cheaper on a pure cost basis before flexibility or tax considerations apply.

✓ You lack a dedicated internal IT resource. Without an internal IT team for setup, maintenance, and support, the hidden cost of ownership escalates rapidly. A managed lease from AMR Technosoft transfers all of this responsibility — configuration, support, replacement, and end-of-life — at zero marginal cost.

✓ Your capital generates returns above 18%. Most growth-stage Indian businesses can deploy capital at returns above the effective “cost” of laptop ownership. When this is true, the opportunity cost of capital alone justifies leasing — even if the direct costs were equal.

✓ You want current-generation hardware throughout. Leasing guarantees access to current-generation equipment at each renewal. Purchasing locks you into the spec that was current at purchase — which may be significantly underpowered 24–36 months later as software requirements grow.

AMR Technosoft Recommendation

For most Indian businesses, long-term leasing is both the financially and operationally superior choice.

Our analysis of 1500+ client deployments consistently shows that businesses which lease their laptop fleet spend 25–35% less on IT hardware over 3 years, while gaining operational flexibility, current hardware, zero maintenance overhead, and complete predictability of IT costs. The recommendation is not universal: stable organisations with strong internal IT and 4+ year device lifecycles may find ownership advantageous. But for the majority of Indian businesses — and almost all growth-stage companies — the TCO analysis is decisive in favour of leasing.

Conclusion: The Numbers Don’t Lie

The financial case for long-term laptop leasing is not a marketing narrative — it is a mathematical outcome. When every cost of laptop ownership is properly identified and quantified, and compared against the all-inclusive cost of a managed lease, leasing emerges as the financially superior option for the majority of Indian business use cases across the 12–36 month planning horizon.

The average Indian business switching from purchasing to leasing a 20-device laptop fleet saves ₹2,80,000–7,20,000 over 24 months — while eliminating maintenance risk, removing IT support overhead, gaining access to current-generation hardware, and preserving capital for revenue-generating deployment.

The businesses that resist this conclusion most strongly are typically those that have never run a complete TCO analysis — comparing the lease payment to the purchase price rather than to the true ownership cost. Once that comparison is corrected, the decision almost always changes.. If the result surprises you, you are in the 67% of businesses that have been underestimating their ownership cost. The next step is a conversation with AMR Technosoft — where a same-day quote will translate this analysis into a concrete, actionable proposal for your specific fleet requirement.